25 min read

On this page

- + A Fairfield buyer meets the two-hit system

- + How Connecticut vehicle tax actually works

- + The sales tax and luxury surcharge

- + The annual property tax: assessment, mill rates, depreciation

- + Five-year cost: Hartford vs Greenwich vs Montana LLC

- + Who gets hit hardest in Connecticut

- + The Montana LLC solution

- + Is this actually legal in Connecticut?

- + Three Connecticut case studies

- + Our process: from sign-up to plates

- + Connecticut vehicle tax FAQs

- + Ready to stop overpaying?

A Fairfield buyer meets the two-hit system

Connecticut vehicle tax is the kind of bill that arrives in two parts, and the second part is the one that breaks people. The first part, you see coming. You sit at the dealership, you sign the papers, and you watch sales tax get tacked onto the bottom of the deal. You grit your teeth. You drive home. You think it is over.

It is not over. It is barely starting.

Meet Daniel. Daniel is a 47-year-old wealth manager who lives in Fairfield with his wife and two kids. In the spring of 2025 he walks into a dealership and orders a 2025 Porsche Cayenne GTS. The window sticker reads $95,400. He pays cash. The finance office runs the numbers, and because the vehicle crosses the magic $50,000 threshold, the entire purchase price gets hit with the 7.75 percent luxury rate. That is $7,394 in sales tax handed to the Connecticut Department of Revenue Services on day one. Daniel groans, signs, and tells himself he is done.

He is not done. Eight months later a yellow envelope shows up in the mailbox from the Town of Fairfield Tax Collector. He opens it on the kitchen counter while the coffee is brewing. The envelope contains a motor vehicle property tax bill. The number on it is $2,128. For one year. On a car he has already paid taxes on. On a car the state had nothing to do with manufacturing, financing, insuring, or fueling. The town simply assesses the Cayenne, applies a depreciation table, multiplies by a mill rate, and bills him every single year that he owns the vehicle. The bill will keep coming. It will arrive next year and the year after that, smaller each year as the depreciation schedule grinds the assessment down, but it will not stop until the car is sold or twenty years pass and the assessment hits the $500 floor. Daniel does the math standing in his kitchen and realizes he is on the hook for roughly $9,500 in property tax over the next five years on top of the $7,394 he already paid in sales tax. Total Connecticut tax burden on a single Porsche over five years: just under $17,000.

This is what Connecticut vehicle tax looks like when you actually run the numbers. It is the only kind of tax bill in the country that says, in effect, you do not really own this car. You rent it. From the town. Forever.

How Connecticut vehicle tax actually works

Most states pick a lane. They charge sales tax at purchase, or they charge an annual registration fee, or they charge a property tax through the local government. Connecticut decided to do all three at once. When you buy a vehicle, you pay state sales tax to the Connecticut Department of Revenue Services. Then you register through the Connecticut DMV and pay a registration fee, $120 every three years for a standard passenger vehicle. Then, every single October, the town where you live assesses the vehicle as personal property and sends you a tax bill. That third piece is the one that turns Connecticut vehicle tax from an annoyance into a wealth-extraction system.

The legal mechanism is straightforward. Connecticut municipalities are authorized to levy a personal property tax on motor vehicles owned by residents. Each town has an assessor who values the vehicle at 70 percent of MSRP, applies a depreciation schedule that drops 5 percent per year until it bottoms out at a $500 minimum, and then multiplies that assessed value by the town’s motor vehicle mill rate. The result is your annual bill. Pay it by the deadline or you lose the ability to renew your registration. Pay it late and Stamford, for example, charges 18 percent annual interest on the overdue balance.

What makes the system particularly rough is that the property tax has nothing to do with how often you drive the vehicle, how much it weighs, what fuel it uses, or what its emissions are. It is purely a tax on owning the asset. A Porsche that sits in a heated garage for ten months and gets driven on weekends in October pays exactly the same property tax as a Porsche that gets daily-driven across the I-95 corridor. The town is not taxing you for road wear. The town is taxing you because the car exists in its boundaries on October 1.

The 2025 reform helped some towns and not others. Public Act 22-118, refined further in 2025, set a statutory cap that says no municipality’s motor vehicle mill rate can exceed 32.46 mills, and as of July 2025, no town’s motor vehicle mill rate can exceed its lowest real estate mill rate for that year. That second rule was a meaningful win in places like Greenwich, Westport, and Darien, where real estate mill rates run very low and the new floor for the MV rate dropped accordingly. But in Hartford, New Haven, and a stack of other working-class cities, the real estate rate is so high that the cap of 32.46 mills is the binding constraint, and the binding constraint is brutal.

The sales tax and luxury surcharge

The first hit in the Connecticut vehicle tax structure is the sales tax. The state charges 6.35 percent on vehicles priced at $50,000 or under. On vehicles priced at $50,001 or above, the rate jumps to 7.75 percent. This is the part that catches a lot of buyers off guard, because the higher rate applies to the entire purchase price, not just the amount over $50,000. So if you buy a vehicle for $49,999, you pay 6.35 percent. If you buy the same model for $50,001, you pay 7.75 percent on the whole thing. That two-dollar difference at the sticker level can cost you $700 in sales tax. A buyer who negotiates the price from $50,400 down to $49,900 saves the dealer commission and saves themselves $700 in tax.

For luxury and performance vehicles this matters enormously. Almost any new full-size SUV crosses the threshold. So does almost any European sport sedan. So does almost any half-decent pickup truck once you start adding option packages. A loaded Ford F-150 Platinum, a Mercedes GLE, a BMW X5, a Range Rover Sport, a Porsche Macan with options, a Tesla Model X, and most three-row SUVs all land in luxury-rate territory. The 1.4 percentage point premium becomes very real money very fast.

Private party trap: if you buy a used vehicle from a private seller in Connecticut, the sales tax is calculated on whichever is higher: the bill of sale OR the NADA average trade-in value. You cannot simply write $5,000 on the bill of sale for a vehicle the NADA guide values at $18,000 and pay tax on the lower number. The DMV pulls the NADA value, compares, and bills you on the higher figure. There is also no trade-in credit on private party deals, which differs from dealer transactions where the trade-in deduction is allowed.

That private party rule catches a lot of in-state used buyers off guard. They negotiate a great deal, exchange paperwork, and arrive at the DMV expecting to pay sales tax on the agreed price. Instead, the clerk pulls up the NADA value, applies the higher figure, and hands them a tax bill that is hundreds of dollars more than they expected. There is no appeal. The system is designed to prevent under-reporting, and it is enforced consistently.

Sales tax is a one-time event. You write the check, you walk away, and the state has no further claim on that vehicle. If sales tax were the entire Connecticut vehicle tax story, the state would be roughly average. It is the second hit, the recurring municipal property tax, that pushes Connecticut into the worst-in-the-country tier.

The annual property tax: assessment, mill rates, depreciation

The Connecticut vehicle tax property bill is calculated with three numbers: MSRP, depreciation percentage, and mill rate. The town assessor starts with the manufacturer’s suggested retail price. Not what you actually paid. Not Kelley Blue Book. MSRP. That number is then multiplied by 70 percent to produce the assessed value, which is then run through a depreciation schedule that drops 5 percent per year. Year one assesses at 80 percent of MSRP. Year two at 75 percent. Year three at 70 percent. The schedule continues stepping down 5 percent per year until it reaches the floor of $500, which generally happens around the twenty-year mark.

Once the assessed value is established, the town multiplies it by the motor vehicle mill rate, divides by 1,000, and that is your bill. The mill rate is the variable that changes everything. A vehicle that costs $65,000 in Hartford is taxed at the statutory cap of 32.46 mills. The exact same vehicle in Greenwich is taxed at 12.041 mills. The bill in Hartford is roughly two and a half times higher than the bill in Greenwich on the same physical car. Same MSRP, same depreciation table, same state. Different town. Different math.

The dirty little secret of the new 2025 rule is that it gave a tax cut to the wealthiest towns and did almost nothing for the cities where ordinary working families live. Greenwich’s motor vehicle bill on a $65,000 SUV dropped meaningfully. Hartford’s bill on the same vehicle did not move at all. The constitutional logic is fine. The real-world result is that Connecticut’s vehicle tax burden is regressive: the people who can least afford it are paying the most.

The depreciation schedule itself is worth understanding because it is the reason your bill never actually goes to zero. After year one at 80 percent, the schedule drops 5 percentage points each year. By year five you are still being assessed at 60 percent of MSRP. By year ten, roughly 35 percent. By year fifteen, about 10 percent. Only when you cross the twenty-year mark does the assessment hit the $500 floor. A daily driver you paid for in cash twelve years ago still generates a town tax bill every October. That is the core of the Connecticut vehicle tax problem. The bill never really stops.

Five-year cost: Hartford vs Greenwich vs Montana LLC

Here is what the actual money looks like over a five-year holding period across three vehicle prices. The Hartford column assumes the 32.46 mill statutory cap. The Greenwich column assumes the 12.041 mill rate that applies under the new 2025 lowest-real-estate-rate floor. The Montana LLC column assumes year one at $899 (which includes the $699 service plus $200 LLC filing) and years two through five at $270 per year (which is $150 registered agent plus $120 annual report).

$65,000 vehicle

$95,000 vehicle

$130,000 vehicle

The bottom line: on a $95,000 vehicle, a Hartford resident pays just over $18,000 in Connecticut vehicle tax over five years. The same vehicle on Montana plates costs $1,979 over the same period. That is more than $16,000 in savings on a single vehicle. Greenwich residents save closer to $9,400 over five years. The savings scale with the price of the vehicle and the mill rate of the town.

Who gets hit hardest in Connecticut

The Connecticut vehicle tax does not hit everyone equally. Some buyers and some lifestyles get destroyed by it. Four profiles show up most often in our intake calls from Connecticut residents.

The Hartford luxury buyer

This is the textbook worst-case scenario. You live in Hartford, West Hartford, or any of the inner-ring towns where the mill rate is at or near the 32.46 cap. You drive a vehicle that crosses $50,000, so you took the 7.75 percent sales tax hit at purchase. Now every October, the town runs your VIN through its assessment system, applies the depreciation schedule against your MSRP, and bills you. On a $95,000 SUV in Hartford, year one alone is roughly $2,467 in property tax. Five-year total tax burden, including sales tax, lands somewhere north of $18,000. The same vehicle through a Montana LLC runs $1,979 over the same five years.

The private party used car buyer

You found a clean used Toyota 4Runner or Tacoma on Facebook Marketplace from a neighbor who is moving. You agreed on $22,000. You show up at the DMV expecting to pay sales tax on $22,000. The clerk runs the NADA average trade-in value, which says $26,400. You pay sales tax on $26,400. Worse, that vehicle now generates property tax bills every October from your town. There is no escape valve. Private party buyers in Connecticut face the same recurring tax obligations as new car buyers, but without the warranty, the financing rate, or the ability to deduct a trade-in.

The multi-car household

Connecticut vehicle tax is per-vehicle. A family with three drivers and three vehicles pays property tax on three vehicles. If you have a daily driver, a weekend toy, and a teenager’s car, you generate three October bills every year. If you live in Hartford and your three vehicles are valued at $30,000, $55,000, and $20,000, your year-one property tax bill alone runs around $2,750 just to keep all three legally registered. That is a recurring four-figure annual expense that does not exist in most other states.

The snowbird and the RV owner

You have a 40-foot Class A diesel pusher you bought for $250,000. You take it south every winter. You drive it for ten weeks a year. The town does not care. The vehicle is registered in Connecticut, the assessor sees it on the rolls, and the mill rate gets applied to the same depreciation schedule as a daily-driven sedan. Year one assessment: $200,000 (80 percent of MSRP). At Hartford’s 32.46 mills the year-one property tax alone is $4,544 plus the original $19,375 sales tax. RV owners, snowbirds, and seasonal collectors get punished hardest because the tax has zero relationship to actual usage.

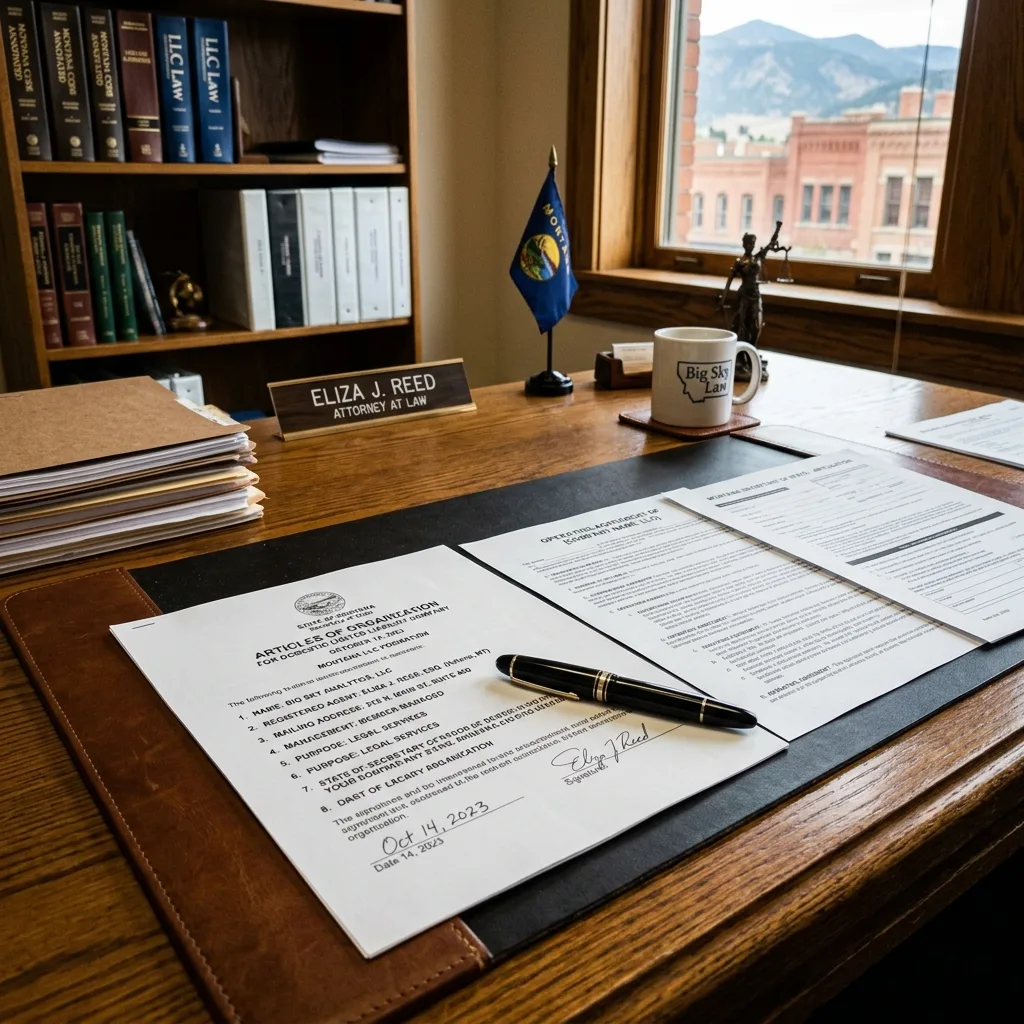

The Montana LLC solution

The Montana LLC strategy works because of how Montana titles vehicles. Montana has no state sales tax. Zero. Not on cars, not on RVs, not on motorcycles, not on anything. Montana also charges a flat registration fee instead of a property tax tied to vehicle value. And Montana, like every other state, allows limited liability companies to own vehicles and register them in the company name.

Put those three facts together and you have the strategy. You form a Montana LLC. The LLC takes title to the vehicle. The LLC registers the vehicle in Montana. Montana issues plates. The plates are real, the title is real, the registration is real, and the LLC is a real Montana entity in good standing with the Secretary of State. There is no sales tax to pay because Montana does not charge one. There is no annual property tax because Montana does not charge one. The annual cost of keeping the LLC alive is the registered agent fee plus the annual report fee, which together total $270 per year.

Your year-one cost through Zero Tax Tags is $899. That breaks down as $699 for our service (which covers the LLC formation, the title transfer, the Montana DMV registration, the title work, and the plate issuance) plus $200 for the actual Montana state filing fee. From year two onward you pay $270 per year, which is the $150 registered agent retainer plus the $120 annual report. After five years you have spent $1,979 total. That is less than one year of Connecticut property tax on a luxury SUV in Hartford.

What you avoid: Connecticut sales tax of 6.35 percent or 7.75 percent on the entire purchase price. Annual Connecticut municipal property tax based on MSRP, depreciation schedule, and town mill rate. The 18 percent late-payment interest some Connecticut towns charge. The proposed tripling of EV registration fees from $120 to $345 every three years under HB 5568. The administrative friction of dealing with both the Connecticut DMV and your local town tax office.

The numbers compound when you own multiple vehicles. A household with three vehicles in Hartford on Montana plates still pays $1,979 in service fees over five years for the LLC, not $1,979 per vehicle. The LLC owns all three. One entity, one set of fees, multiple vehicles. The savings curve gets steeper with every vehicle you add.

Is this actually legal in Connecticut?

This is the question every Connecticut buyer asks first, and the honest answer is more nuanced than a simple yes or no. Forming a Montana LLC is legal. Titling a vehicle to a Montana LLC is legal. Registering that vehicle in Montana is legal. The Montana DMV issues legitimate plates and a legitimate title to the LLC. None of those facts are in dispute. The structure has been used by collectors, RV owners, and high-net-worth individuals for decades, and it survives because every step of it is grounded in real corporate law and real state titling rules.

Where the analysis gets sharper is in how Connecticut treats vehicles owned by out-of-state entities and how often a vehicle on Montana plates physically operates within Connecticut. The strategy works cleanly for vehicles that are not principally used as Connecticut daily drivers. RVs, motorhomes, exotic and collector cars, weekend toys, second and third vehicles in a multi-car household, classic cars in storage, race cars, and seasonal vehicles are the textbook fits. They sit in storage or on the road across multiple states, and the Montana LLC owns them as a real entity.

What the strategy does not do is give a single-vehicle Hartford resident license to evade their daily-driver registration obligation. There are jurisdictions and edge cases where state revenue departments have pushed back. We always recommend a frank conversation about your usage pattern before you sign anything, and we always tell prospects who do not fit the profile that they do not fit the profile. We do not take clients we cannot help.

The bottom line: Montana LLC vehicle ownership is legal at the federal and Montana levels and has been used at scale for decades. The fit with your specific situation is what we evaluate during the intake call.

Three Connecticut case studies

The West Hartford attorney

A 52-year-old partner at a downtown firm bought a 2024 Mercedes-AMG GT 63 S in late 2024 with an MSRP of $178,000. His sales tax hit at purchase: $13,795 at the 7.75 percent luxury rate. His first West Hartford property tax bill arrived the following October at $4,617 against an assessed value of approximately $142,400. That was year one. The car was a weekend driver. He drove it perhaps 4,000 miles annually. He lived next door to a colleague who had structured a similar weekend toy through a Montana LLC and had paid roughly $900 to set up the entity for a vehicle that had never seen a sales tax bill or a property tax bill since. After running the math on his five-year hold, the West Hartford attorney moved his next purchase, a 2026 Porsche 911 GT3, into a Montana LLC structure from day one. Estimated five-year savings on the GT3 alone: $24,000.

The Fairfield contractor with the F-350

A construction business owner in Fairfield bought a new 2025 Ford F-350 Platinum dually with an as-built sticker price of $96,500. He used the truck for hauling equipment between job sites in Connecticut, New York, and Massachusetts. Sales tax at the 7.75 percent rate was $7,479 on the day he took delivery. His Fairfield property tax bill in year one came to roughly $2,154 at the 27.9 mill rate. Because the vehicle was a true business asset that operated across state lines, his accountant routed him to a Montana LLC structure where the LLC took title and the truck registered on Montana commercial plates. Five-year tax savings versus continuing on Connecticut plates: about $14,300, plus a much cleaner accounting trail because the asset and its expenses now lived inside a single dedicated entity.

The Westport couple with the motorhome

A retired Westport couple, both 64, bought a $312,000 Newmar Dutch Star motorhome to spend winters in Florida and summers visiting grandkids in Vermont and Maine. Sales tax in Connecticut at the 7.75 percent rate would have been $24,180 at purchase. The motorhome would have generated annual Westport property tax bills of around $3,000 in year one (Westport mill rate around 12.5 mills under the new rule). Across a five-year hold, total Connecticut tax burden on the motorhome would have run more than $35,000. They formed a Montana LLC before purchase, took delivery in Montana, registered on Montana commercial plates, and paid $899 for year one and $270 per year thereafter. Five-year tax savings: just over $33,000. They use the savings to fund their fuel and campground costs for two full winters in the Florida Keys.

Our process: from sign-up to plates

From the moment you decide to move a vehicle to Montana plates, the timeline runs roughly two weeks.

| Day 1: | Discovery call. We walk through your vehicle, your usage pattern, your residence, and the savings math. You decide to move forward and we send the engagement letter. |

| Day 2: | LLC formation. We file the Articles of Organization with the Montana Secretary of State. The state generally approves in 24-48 hours. Your registered agent is assigned. You receive your Montana LLC EIN if needed. |

| Day 3-7: | Title transfer. We prepare the Montana title application and the bill of sale assigning the vehicle from you (or from the dealer) to your new LLC. You sign and notarize the documents and overnight them back to us. |

| Day 7-14: | Montana DMV processing. We file the title and registration paperwork with the appropriate Montana county treasurer’s office. Plates and registration are issued and shipped directly to you. You receive Montana plates, registration card, and a clean Montana title in the LLC name. |

| Year 2+: | Annual maintenance. We file your Montana annual report and renew your registered agent retainer for $270 total per year. We also handle the registration renewal cycle and forward any official mail. You do nothing. |

Total touch time on your end is generally about two hours of paperwork and a couple of trips to a notary. Total elapsed time from sign-up to plates in your hand is two weeks. Total cost in year one is $899. We do this hundreds of times per year. The process is dialed in.

Connecticut vehicle tax FAQs

Do I really have to pay both sales tax and annual property tax in Connecticut?

Yes. Connecticut is one of fewer than two dozen states that levy a recurring municipal property tax on personal-use vehicles, and it does so on top of the state sales tax assessed at purchase. The two taxes are separate, governed by different statutes, and collected by different agencies (the state Department of Revenue Services for sales tax and your local town tax office for property tax).

What is the mill rate cap and how does the new 2025 rule work?

Connecticut caps motor vehicle mill rates at 32.46 mills statewide. As of July 2025, no town’s motor vehicle mill rate may exceed its lowest real estate mill rate for that year, whichever is lower. In low-real-estate-rate towns like Greenwich and Westport, this dropped the MV rate well below 32.46. In Hartford and New Haven, where real estate rates exceed 60 mills, the cap of 32.46 mills is the binding constraint.

How is my vehicle assessed if I bought it used or for less than MSRP?

For property tax purposes, Connecticut towns assess at 70 percent of MSRP run through the depreciation schedule. The fact that you paid less than MSRP does not change the property tax assessment. For sales tax on private party purchases, the higher of the bill of sale or the NADA average trade-in value applies.

What happens if I move into Connecticut from another state?

You become liable for Connecticut sales tax on the vehicle (offset by sales tax already paid in the prior state, in most cases) when you register it here, plus you become liable for the annual municipal property tax based on the assessment as of October 1 of the year you register. New Connecticut residents are routinely surprised by the property tax obligation in their first October.

Can I just register my car in another state to avoid the property tax?

Not legally if you are a Connecticut resident driving the car as a daily driver. The Montana LLC structure works because the LLC, not you personally, owns the vehicle, and the structure is designed for specific use cases (RVs, second vehicles, collector cars, business vehicles). Speak with us about whether your situation fits.

Do EVs pay property tax in Connecticut?

Yes. EVs are taxed identically to gas vehicles for both sales tax and municipal property tax purposes. There is also a current $120 per three-year EV registration fee, and HB 5568 (introduced March 2026) proposes to triple that fee to $345 per three years. Plug-in hybrids are proposed to move to $233.

What is the deadline for paying my motor vehicle property tax?

Most Connecticut towns set the motor vehicle property tax due in two installments, typically July and January, on the prior October 1 grand list. Miss a deadline and interest begins accruing immediately, often at 1.5 percent per month (18 percent annualized). Unpaid taxes will block your registration renewal at the Connecticut DMV.

What if I sell or junk my car mid-year?

Connecticut allows a property tax credit or refund for vehicles sold, totaled, or removed from the state during the assessment year, but you must file the proper documentation with your town assessor (typically a copy of the bill of sale or the disposal receipt). The refund is prorated. If you do not file, you owe the full year.

How quickly can Zero Tax Tags get me on Montana plates?

From signed engagement letter to plates in your hand is typically 10 to 14 days. The LLC formation step takes 24-48 hours, the title transfer paperwork takes about a week, and Montana DMV processing takes another week. We have completed faster timelines for clients with delivery deadlines.

Does the Montana LLC affect my Connecticut auto insurance?

You will need an insurance policy that lists the Montana LLC as the registered owner and you as the named driver. Most major carriers accommodate this. We work with insurance brokers who specialize in Montana-titled vehicles and can provide referrals during the onboarding process.

Ready to stop overpaying?

Connecticut vehicle tax is a uniquely punishing structure. The state hits you at the dealership with one of the highest sales tax rates in the Northeast, then your town hits you every October for as long as you own the vehicle. Five years of ownership on a $95,000 vehicle in Hartford costs over $18,000 in combined Connecticut vehicle tax. The same vehicle through a Montana LLC costs $1,979. The math is not subtle.

You can keep opening yellow envelopes from your town tax collector every October. You can keep watching the depreciation schedule grind down at five percentage points a year while the bill keeps coming. Or you can move your next vehicle, your weekend toy, your motorhome, or your collector car onto Montana plates and stop the bleeding for $899 in year one.

For a deeper look at the Connecticut DMV’s role in registration and property-tax verification, you can review the official Connecticut DMV portal at portal.ct.gov/dmv.

See how Montana LLC registration helps owners in other high-tax states:

- Arizona VLT Problem: How to Stop Paying $1,000 Every Single Year

- Virginia Car Tax: Stop Paying the Highest Vehicle Tax in America

- Nevada’s 8.25% Car Tax: The Hidden Cost Nobody Tells You About

- Texas Vehicle Tax: The 6.25% MVST, SPV Trap and RV Gotcha

Ready to stop overpaying Connecticut vehicle tax?

Connecticut vehicle owners have saved thousands with Montana LLC registration. Year one is $899. Year two and beyond is $270.