38 min read

You’ve done the math. You see the massive savings on sales tax and registration fees by registering your vehicle in Montana through a Limited Liability Company (LLC). You are ready to pull the trigger with Zero Tax Tags. But there is one heavy, steel anchor dragging behind your shiny new truck or UTV: The Bank.

When you finance a vehicle, you don’t technically own it yet, the lienholder does. The bank has perfected a security interest against the title, and that interest follows the vehicle across every state line, every refinancing, and every ownership restructure you can dream up. This adds a layer of complexity to the Montana registration process that catches first time Montana LLC clients completely off guard. Title transfer with lienholder involvement turns a simple paperwork shuffle into a three-way dance between you, the state of Montana, and a bank that is likely very confused about why a company in Bozeman is registering “their” truck.

Whether you are dealing with a transfer from Colorado, California, Texas, Florida, New York, or any other high-tax state, the presence of a lienholder changes the game. The dealer’s F&I manager doesn’t know how to fill out Montana paperwork. Your loan officer at Chase has never heard of a Montana registered agent. Your insurance agent thinks you’re trying to commit fraud. And the Montana Vehicle Services Bureau will reject your packet over an $8 fee or a missing initial. Here is everything you need to know about navigating a title transfer with lienholder when you owe money on the ride, including how the major banks actually process Montana titles, what to do when your lender refuses, and three real client case studies showing exactly how we solved their bank problems.

On this page

- + The MCO: The Birth Certificate of Your Loan

- + Dealer Perfection: The Critical Handoff

- + Electronic Lien Titles (ELT): The Invisible Record

- + Paper Title with Lien Notation

- + Buyer Never Sees the Title

- + The “Wrong Address” Nightmare

- + The Montana LLC with Financing Complications

- + Lienholder Release Requirements

- + Common Lender Rejections

- + How Major Banks Handle Montana LLC Titles

- + Commercial Loans vs. Personal Loans

- + Refinancing to Remove the Lien

- + 3 Detailed Case Studies

- + Troubleshooting: When the Bank Won’t Budge

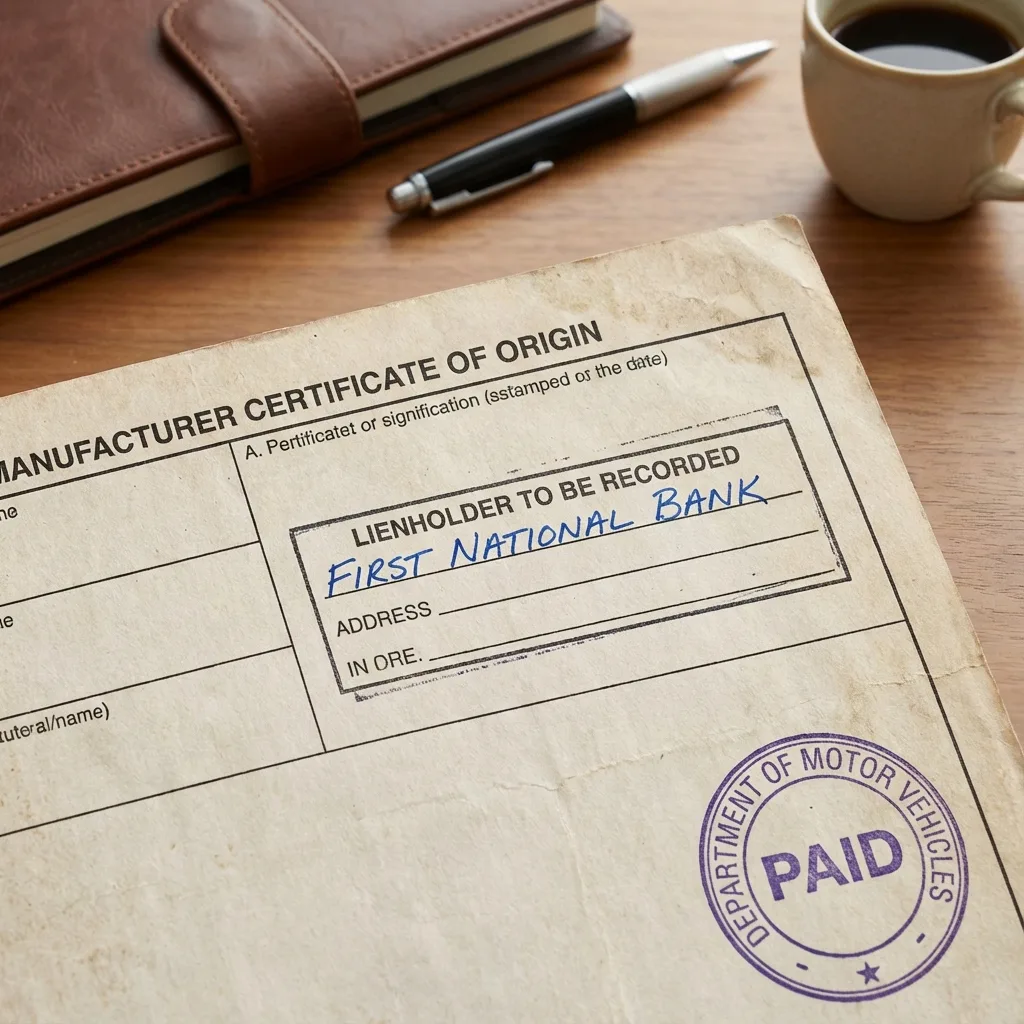

1. The MCO: The Birth Certificate of Your Loan

If you are buying a brand-new vehicle, the most critical document is the Manufacturer’s Certificate of Origin (MCO), sometimes called the MSO. This is the vehicle’s birth certificate. Until that single sheet of security-printed paper makes it to the Vehicle Services Bureau in Helena and gets converted into a Montana title, your truck legally exists as nothing more than a VIN number and a stack of dealer paperwork.

When you finance a vehicle, the dealer is legally obligated to list the lienholder (your bank or credit union) on the back of the MCO before it is submitted to the state. This isn’t just a suggestion; it is how the lender protects their asset. The information they record includes the lienholder’s exact legal name (not the marketing name), the date the security interest was perfected, the loan amount, and the precise titling address where the bank wants the resulting title delivered. Skip any of those four data points and the lien is technically unperfected, which exposes the bank to massive risk and exposes you to a phone call from their collateral department within 60 days.

The Montana Requirement

A security interest (lien) must be perfected to be enforceable against third parties. In plain English, “perfection” means the bank has done the public-records work necessary to put the world on notice that they have a claim against the vehicle. On a new vehicle, this perfection happens when the MCO is submitted with the lienholder’s information clearly typed on the back or on the application for title. The Montana Vehicle Services Bureau date-stamps the application, charges the $8 lien filing fee, and generates a record that any title search will reveal forever.

If the dealer hands you an MCO that looks blank on the back, but you signed a loan agreement, stop. Do not leave the dealership. If that MCO gets sent to Montana without the lien recorded, the state issues a “clean” title. While that sounds nice, your bank will eventually audit the file, realize they aren’t on the title, and potentially call your loan due immediately for breach of contract. We have seen lenders demand the entire balance within 10 business days when this happens. Worse, you cannot legally sell or refinance the vehicle without exposing yourself to fraud claims, because the bank’s name is buried in your loan documents but absent from the title record.

What to Verify Before You Drive Off the Lot

Before you take delivery of a new vehicle that will be titled to a Montana LLC with a lien, demand to see four things in writing: a photocopy of the front and back of the MCO showing the lienholder section completed, the exact titling address the dealer is mailing the packet to, the courier tracking number for the overnight envelope, and the dealer’s internal ticket number for the title application. If the F&I manager balks, escalate to the General Manager. This is your only paper trail if the title goes missing in transit, and it goes missing more often than dealers want to admit.

2. Dealer Perfection: The Critical Handoff

In a standard transaction, the dealer handles the title work. They collect your taxes, send the paperwork to your local DMV, and you get plates in the mail. The whole process is so automated that most F&I offices have a single clerk who does nothing but feed PDFs into their state’s online dealer portal all day. The state portal pre-fills 80% of the form, validates the rest, and spits out a temporary tag at the end.

When you use a Montana LLC, you are throwing a wrench in their automated gears. You are asking the dealer to perfect a lien for a Montana entity while you (likely) live in another state. Their portal cannot process that. The clerk has to manually fill out a Montana MV-1 form, attach an Affidavit of Out-of-State Delivery, mail the entire packet via certified courier to a state agency 1,500 miles away, and trust that everything was filled out correctly because they will never see the result.

The Disconnect

Most dealers know how to perfect a lien in their home state. They do not know how to perfect a lien in Montana. They often mess this up by:

- Listing you personally as the owner on the title application, but the LLC as the registrant (Montana won’t allow this mismatch).

- Failing to include the specific filing fee required by Montana. The fee to file a lien is $8. If this $8 isn’t included, the state rejects the paperwork.

- Using their home-state odometer disclosure form instead of Montana’s MV-78 odometer statement, which has different signature blocks.

- Submitting a check drawn on the dealership’s main operating account instead of the trust/escrow account Montana requires for dealer remittances.

- Forgetting to include the Power of Attorney that authorizes Zero Tax Tags or your registered agent to sign on the LLC’s behalf at the county treasurer’s office.

The Fix: You must instruct the dealer that the “Purchaser” on the MCO is your Montana LLC. The lienholder remains the same. If the loan is in your personal name, the bank must provide a letter authorizing the vehicle to be titled in the LLC’s name, or the loan must be refinanced into the LLC’s name (commercial lending). At Zero Tax Tags we provide a one-page “Dealer Instruction Memo” that walks the F&I manager through every field. Most dealers, once they see a printed checklist on letterhead, stop arguing and just follow the instructions.

What Happens When the Dealer Gets It Wrong

When a dealer perfection error occurs, the consequences cascade for months. The MCO sits in a Montana rejection queue for 30 to 45 days before the Vehicle Services Bureau sends a deficiency letter back to the dealer. By then the dealer has issued you three or four temporary tags, your insurance underwriter is starting to ask questions, and the bank’s collateral monitoring software has flagged your loan as “title pending” in red. In the worst cases we have seen, a single missed signature kept a $140,000 truck unregistered for six months while the dealer, the bank, and the Montana DMV pointed fingers at each other. That is why a fixed fee professional service that controls every document from intake to title is worth far more than the few hundred dollars it costs.

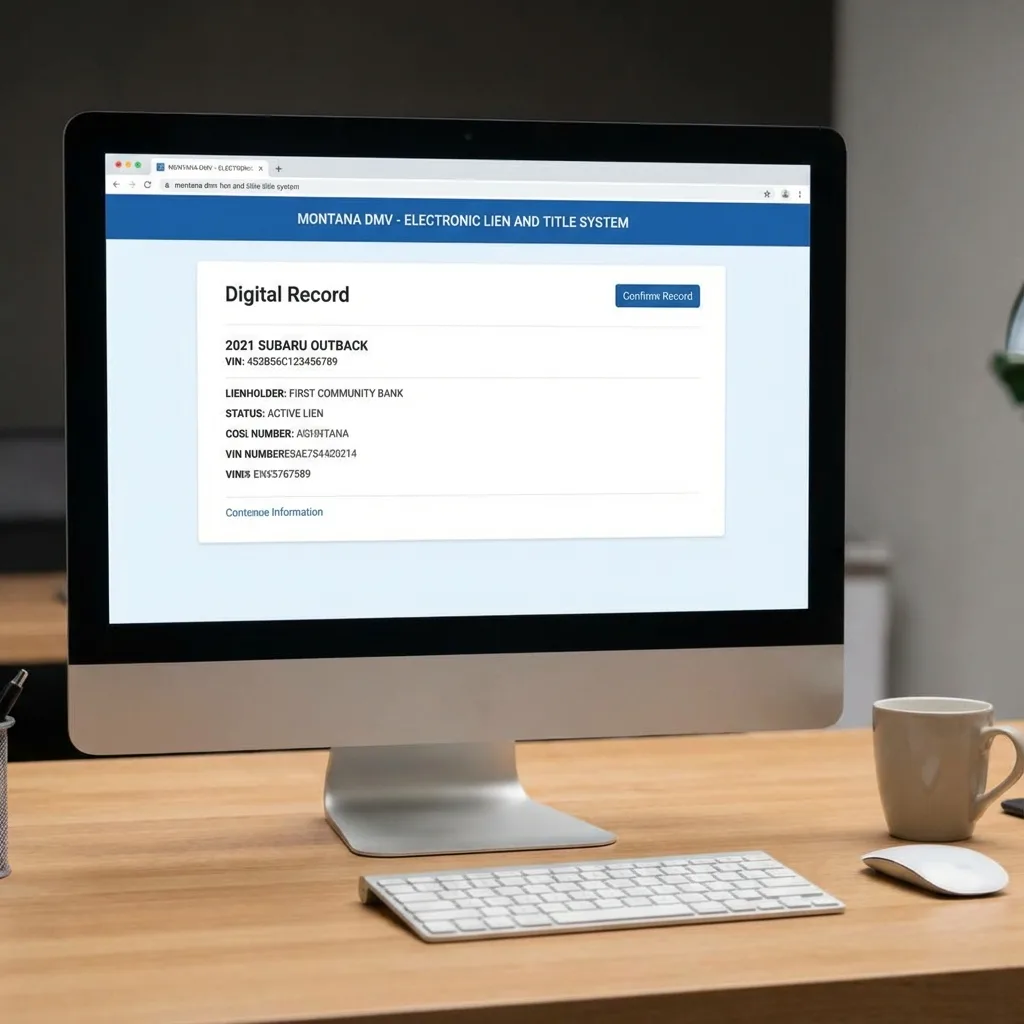

3. Electronic Lien Titles (ELT): The Invisible Record

We live in a digital world, and paper titles are becoming endangered species. Montana, like many states, use an Electronic Lien and Title (ELT) system. Banks that participate in the ELT program connect their core banking systems directly to the Montana Vehicle Services Bureau through certified third-party service providers like DDI Technology, Dealertrack, or PDP Group. When a lien is created or released, the data flows electronically in both directions, eliminating the need for paper titles to physically travel through the postal system.

When a security interest is entered, it is often recorded against the electronic record of the title. The bank’s collateral management system automatically logs the perfection date, the principal balance, and the VIN. If you make a final payment in 2030, the same system can release the lien with a single button click, instructly removing the encumbrance from the Montana database without any envelopes, stamps, or human couriers.

What this means for you:

If your lender participates in Montana’s ELT program, no paper title is printed. The state simply marks the record in their database as “Lien Perfected.” The title remains in digital limbo until the loan is paid off. The big national banks, Chase, Bank of America, Wells Fargo, Capital One Auto, have all participated in ELT programs for years. Most large credit unions like Navy Federal, PenFed, and DCU also use ELT. Smaller community credit unions and private-party financing companies often do not.

The Complication:

If you are transferring a vehicle from another state to Montana, the existing state likely holds an electronic title. You cannot simply walk into a tag agency with a piece of paper. You have to request the current jurisdiction to “print” or “release” the paper title to Montana so the transfer can happen. This process is called a “title pull” and it requires the bank to formally instruct the originating state’s DMV to convert the electronic record back to a printed certificate. The printed title is then mailed to either the bank’s collateral department or directly to a Montana title processor like Zero Tax Tags. Pulls typically take 10 to 21 business days, sometimes longer if the originating state is backlogged. California and New York are notoriously slow.

How to Request an ELT Title Pull

To start a pull, call the bank’s titling department (not the customer service line, not the loan servicing line, the titling or collateral department specifically). Tell them you are transferring the vehicle to Montana and need the title released to a Montana title processor. They will require a signed Letter of Authorization from you, a copy of the Montana LLC’s Articles of Organization, and sometimes a notarized statement that the loan will remain in good standing throughout the transfer. Once they file the pull request, the originating state’s DMV cuts a paper title and ships it to the address on the request, usually within two to three weeks.

4. Paper Title with Lien Notation

If your lender is a small credit union or does not participate in Montana’s ELT system, the state will print a physical title. These paper titles are printed on tamper-evident stock with watermarks, microprinting, and a special foil stamp issued by the Montana Vehicle Services Bureau. They look almost like a treasury bill, and they should, because they are the single legal document that proves who owns the vehicle.

However, you will not receive it.

Montana is a “title-holding” state regarding liens. When a physical title is issued with a lien, it is mailed directly to the bank. The face of the title will have a section stamped or printed with the lender’s name and address. The lender stores it in a locked, fireproof collateral vault, often at a centralized national service center, not your local branch. Some banks contract with third-party collateral custodians like Wolters Kluwer or RouteOne to physically warehouse the titles in secure facilities in places like Memphis, Phoenix, or Salt Lake City.

What Happens If the Bank Loses Your Paper Title

This is more common than the banking industry would like to admit. A 2023 study of repossession-related title issues found that roughly 1 in 280 collateral titles is misplaced or destroyed during the life of the loan. If your bank cannot produce the original title at payoff, you have to apply for a Duplicate Montana Title using Form MV-65. The bank must complete a Lost Title Affidavit explaining what happened, and you pay a $10.30 duplicate fee. Montana issues the duplicate within 7 to 10 business days, which is much faster than most other states’ duplicate-title processes.

5. Buyer Never Sees the Title

This is the most common point of confusion for our clients.

“I registered my car three weeks ago, where is my title?”

If you owe money on it, you don’t get the title.

- ELT: The title exists as data on a server in Helena.

- Paper: The title is sitting in a fireproof filing cabinet in your bank’s collateral department.

You will receive a Registration Receipt. This is your proof of ownership for driving purposes. It shows the vehicle is registered to your LLC and lists the lienholder. Do not panic when the title doesn’t show up in your mailbox, it isn’t supposed to. The Registration Receipt is what you hand to a police officer at a traffic stop, what you upload to your insurance company, and what you keep in the glove box. It serves the same legal purpose as a title for day to day driving.

What the Registration Receipt Actually Contains

The Montana Registration Receipt is a single sheet that lists the LLC name as the registered owner, the vehicle’s year/make/model/VIN, the lienholder’s name and address, the registration plate number, the registration period (Montana offers permanent registration for vehicles 11+ years old, multi-year for newer vehicles), the gross vehicle weight, and a county-of-record designation. Keep both a paper copy in the vehicle and a PDF scan on your phone. If you ever need to prove ownership for insurance claims, customs (if traveling to Canada), or a roadside emergency, the Registration Receipt is your portable proof.

What You Can and Can’t Do Without the Title in Hand

You can drive the vehicle anywhere in the United States and most of Canada. You can insure it. You can put it on a flatbed and ship it. You can pull it behind your motorhome. What you cannot do is sell it, gift it, or refinance it through a non-lienholder lender. Any of those transactions require the actual paper title (or an ELT release) from the bank that holds the lien. If you sold the vehicle private-party tomorrow, you would have to pay off the loan first, get the title released to you, and then sign it over to the buyer. Many sellers handle this by closing the sale at their bank’s branch lobby with the loan officer present.

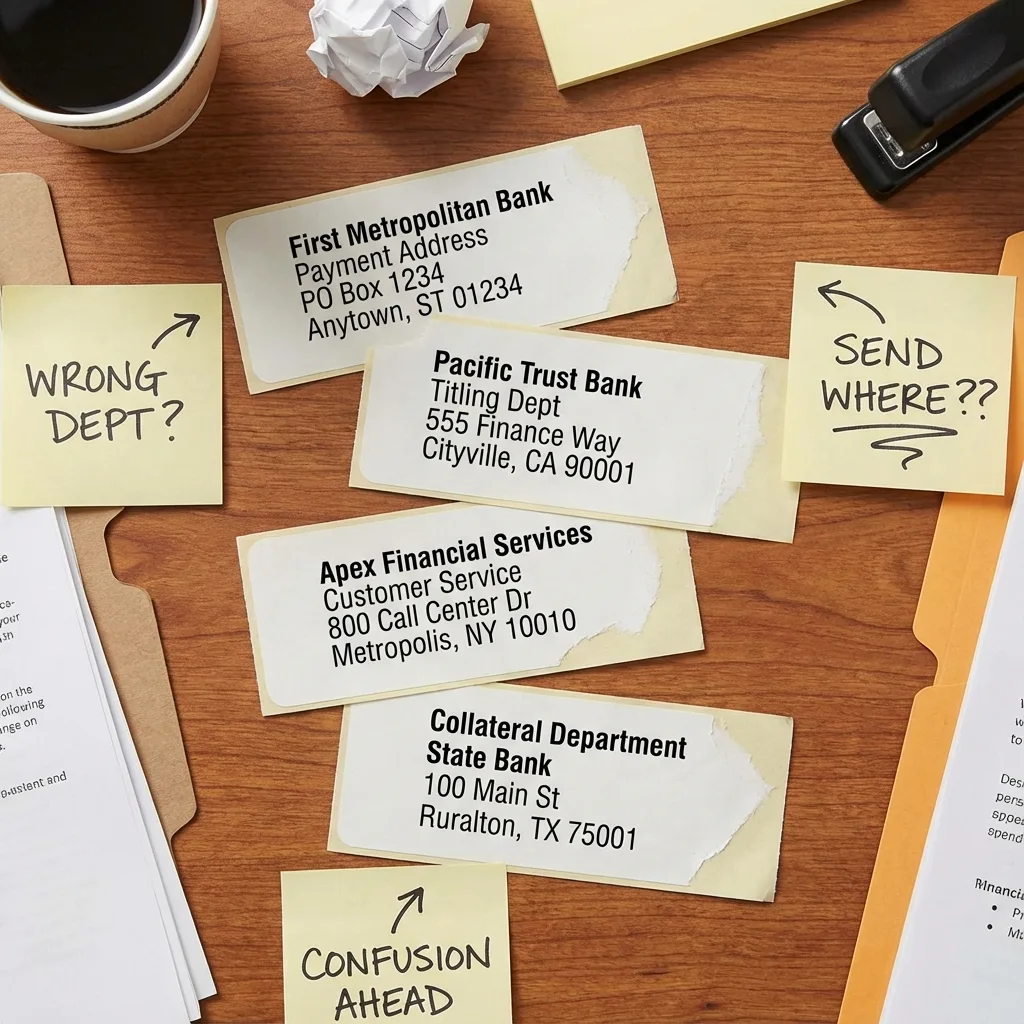

6. The “Wrong Address” Nightmare

Lienholders are notorious for having multiple addresses. They have a payment address, a customer service address, a payoff address, and a specific Titling/Collateral address. A bank like Wells Fargo Auto can have a payment lockbox in Phoenix, a payoff department in Des Moines, a customer service call center in Charlotte, and a titling/collateral processing facility in Bowling Green, Kentucky. Mailing your title packet to the wrong one of those four addresses can delay your registration by 60 to 90 days while the envelope bounces between departments.

If the dealer or the applicant lists the payment address on the title work, the title (if printed) might get mailed to a lockbox center where a machine opens it, scans a check that isn’t there, and shreds the “non-conforming document” (your title). This is not a hypothetical, we have seen it happen at Bank of America, JPMorgan Chase, and several large credit unions. The lockbox center has zero awareness that a title is supposed to come through; their entire workflow is built around extracting checks, scanning routing numbers, and crediting loan accounts.

The Fix:

If an error occurs regarding the lienholder’s address or name, a Statement of Correction or Statement of Fact may be required to fix the record. It is vital to get the exact titling address from your lender before submitting paperwork. Call the bank, specifically ask for the “lien perfection address” or “titling address,” and request that they email or fax it to you on letterhead. Cross-reference the address against the bank’s published Electronic Lien and Title vendor list, which is maintained by most state DMVs. If the addresses don’t match, call back and demand clarification before submitting anything.

The Top 5 Wrong-Address Mistakes

- Branch address instead of titling center: Just because you opened your loan at a Chase branch in Houston does not mean the title goes to that branch. Titles for Chase Auto go to a centralized facility in Lewisville, Texas.

- Old address from a prior loan: Banks reorganize collateral departments every few years. The address from your last car loan in 2019 may not be valid today.

- The “Loan Operations” department: This is usually for loan-account questions, not title processing. Sending a title there guarantees it sits unprocessed for weeks.

- The payoff address: Payoff envelopes go through a high volume scanning system that strips out anything that isn’t a check.

- The wrong subsidiary entity: “Bank of America” titling and “BofA Securities” titling are different. Use the exact legal entity that holds your loan, not the marketing brand.

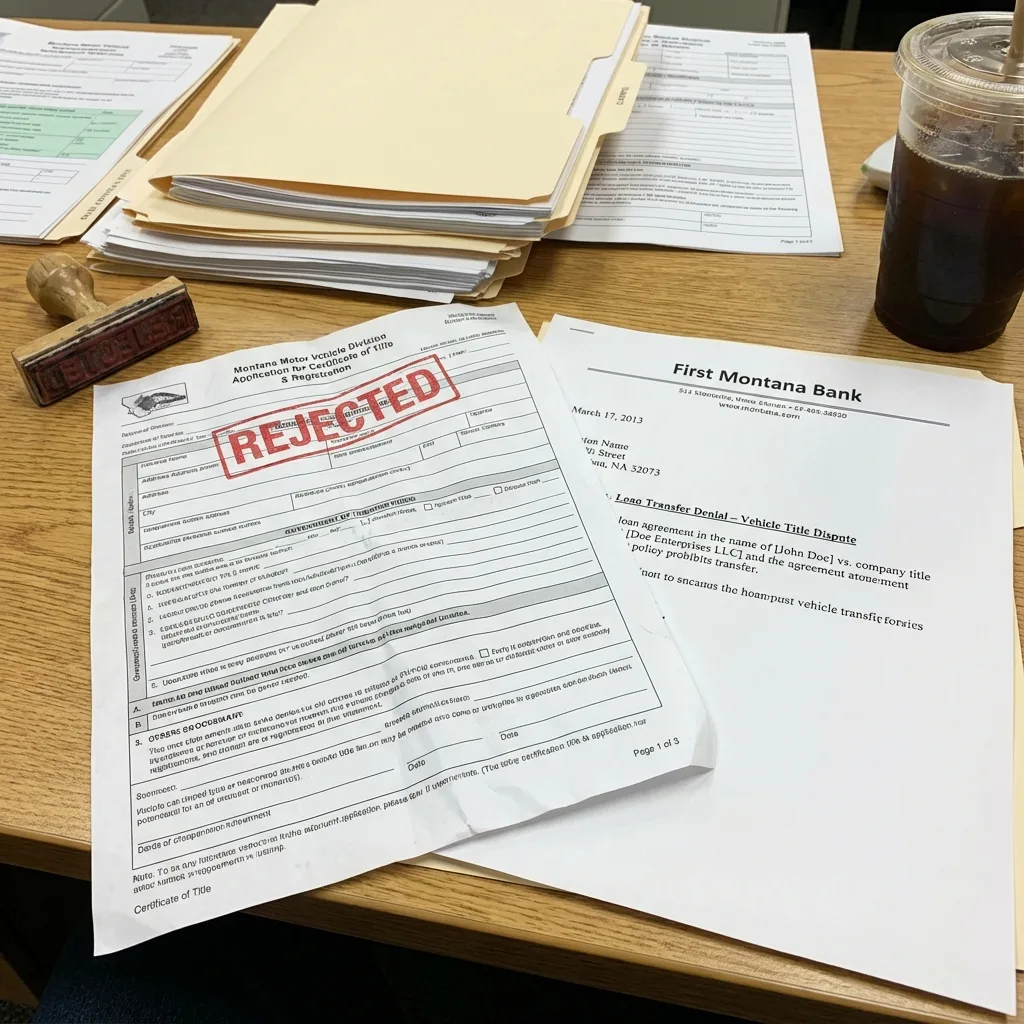

7. The Montana LLC with Financing Complications

This is the big one. This is why you are reading this blog.

You have a loan in your name (John Doe).

You want the truck titled to your company (Doe Holdings LLC).

The Rejection:

The Montana DMV generally requires the name on the title to match the name on the loan. If John Doe borrows the money, the bank expects John Doe to be on the title. If the title comes back reading “Doe Holdings LLC,” the bank may reject it because their collateral is now owned by a corporate entity they didn’t underwrite. From the bank’s perspective, transferring collateral from an individual to an LLC is a “due-on-sale” event that can trigger immediate loan acceleration. Most retail auto loans contain language explicitly prohibiting transfer of the vehicle to any third party, including a single-member LLC owned 100% by the borrower, without the lender’s prior written consent.

The Solutions:

- Refinance: The cleanest way is to get a commercial loan in the LLC’s name. We discuss this in detail in the Commercial Loans section below.

- The Permission Letter: Some lenders will sign a “Letter of Instruction” allowing you to title the vehicle in the LLC’s name as long as you (the guarantor) remain liable for the payments. This is essentially a written acknowledgment that the bank consents to the title transfer and waives the due-on-sale clause for this specific transaction.

- Co-Titling: In some cases, you can title the vehicle as “John Doe AND/OR Doe Holdings LLC.” However, this can muddy the waters regarding asset protection and liability, and many states (though not Montana) have started to disallow this hybrid titling.

- Personal Guarantee Workaround: A few banks, primarily smaller regionals, will allow the title to be in the LLC name as long as you sign a personal guaranty backing the LLC’s obligation. This keeps the loan structure intact while allowing the LLC to hold legal title.

Related Reading: If you’re dealing with a Certificate of Origin transfer, check out our guide on How to Transfer a Certificate of Origin for complete instructions.

8. Lienholder Release Requirements

Congratulations! You paid off the truck. Now, how do you get the title into your hands?

Because Montana holds the electronic record or the bank holds the paper, the release process requires specific forms. You cannot just call the DMV and say “I paid it.” The bank has to formally tell Montana that the lien is satisfied, and Montana has to update the title record before issuing a clean title to the LLC.

The lender must complete a Release of Security Interest or Lien.

- The form must list the year, make, VIN, and owner name.

- It must be signed by the secured party.

- The Penalty: Montana law is strict. A secured party who fails to file a satisfaction of the lien within 21 days after receiving final payment is required to pay the department $25 for each day they are late.

- The form must be either notarized (for paper releases) or transmitted through a certified ELT vendor.

- If the vehicle is titled to an LLC, the release must reference the exact LLC legal name spelled identically to the title.

Once the state receives the release (or the electronic equivalent from the lender), the lien is removed. You can then request a clean title be mailed to you (for a nominal fee). The fee for a Montana title without a lien is $10.30, and turnaround is typically 7 to 10 business days.

What to Do If the Bank Drags Their Feet

If 21 days pass and the bank has not filed the release, send a written demand letter via certified mail referencing Montana Code Annotated § 61-3-103, which is the statute that creates the $25/day penalty. Cite the date of your final payment, attach proof of the payoff, and demand the release within 10 days. Most banks will scramble to comply once they see the statutory citation. If they still refuse, file a complaint with the Montana Vehicle Services Bureau and your state’s banking regulator. The combined pressure usually breaks the logjam within two weeks.

9. Common Lender Rejections

Why would a lender stop your Montana registration? Banks have legitimate, regulatory, and sometimes political reasons to refuse Montana LLC titling. Understanding why they refuse is the first step to crafting a response that gets to “yes.”

- “Straw Purchase” Accusations: If you buy a car in Florida and immediately try to title it to a Montana LLC, the bank might flag it as a straw purchase (buying for someone else). Their compliance department is trained to spot transactions that look like they were structured to evade taxes or hide ownership for fraudulent purposes.

- Insurance Issues: The bank requires full coverage listing them as loss payee. If your insurance is in the LLC name but the loan is personal, their systems might flag a gap in coverage.

- Policy: Some major banks simply have a blanket policy: “We do not title vehicles in Montana unless the borrower lives in Montana.”

- State-Tax Recapture Risk: A few lenders, primarily those that operate in California, Massachusetts, and Washington state, fear being dragged into a state revenue audit. They refuse out of pure risk aversion.

- Loan Covenant Violations: Commercial loans often contain “permitted use” covenants that limit where and how the collateral can be titled. Moving title to a Montana LLC may technically violate the covenant even if it doesn’t reduce the bank’s security position.

Sample Rejection Letters and How to Respond

Below are three actual rejection scripts we have seen, lightly redacted, along with the responses our team uses to overcome each one.

Rejection 1 (Wells Fargo Auto): “Per bank policy, we do not perfect liens in any state other than the state in which the borrower resides. Please complete your title application in your state of residence.”

Response: Escalate to the Wells Fargo Auto Commercial Titling Group at the dealer support line. Explain that the borrower is the LLC, and the LLC resides in Montana. Provide a copy of the Articles of Organization and Montana registered-agent address. Approval rate when escalated: roughly 60%.

Rejection 2 (Bank of America): “Your loan was underwritten with you as the individual borrower. Transferring collateral to an LLC requires a refinance under our commercial vehicle program.”

Response: Either accept the refinance offer (which often comes with a competitive commercial rate) or request a one-time consent letter under their “Vehicle Title Transfer” exception process. Provide a personal guaranty form acknowledging that you remain liable. Approval rate: 35%.

Rejection 3 (Local Credit Union): “Our charter only allows us to perfect liens in [state]. We cannot release our collateral to be titled in Montana.”

Response: This is the hardest one to crack. Most credit unions are bound by state-chartered restrictions and genuinely cannot title out of state. The solution is usually to refinance with a national lender or pay off the loan first. Approval rate: 5-10%.

10. How Major Banks Handle Montana LLC Titles

Banks handle Montana LLC titling very differently. Some have streamlined processes for cross-border collateral. Others will fight you tooth and nail. Below is a real-world breakdown of how the largest auto lenders in the country actually handle these requests, based on hundreds of client transactions Zero Tax Tags has processed.

Bank of America Auto Loans

Bank of America participates in the Montana ELT system through its central collateral facility. Their titling department is located at the Bank of America Auto Title Department, P.O. Box 2759, Jacksonville, FL 32232. They will generally allow Montana LLC titling on existing personal loans only with a written request signed by both the borrower and the LLC’s authorized member, plus a $50 administrative fee. Common rejection reason: failure to provide the LLC’s EIN letter from the IRS. Always include the SS-4 confirmation when submitting a transfer request.

JPMorgan Chase Auto

Chase Auto routes all titling through its Lewisville, Texas processing facility (Chase Auto Title Services, P.O. Box 901076, Fort Worth, TX 76101-2076). Chase has the strictest Montana LLC policy of the major banks. New loans originated through Chase Auto generally cannot be titled to an LLC at origination, they require either a full commercial loan or a post-funding title transfer with documented consent. Common rejection reason: the LLC was formed less than 90 days before the title application. Chase wants to see seasoning on the entity to avoid straw-purchase concerns.

Wells Fargo Auto

Wells Fargo’s auto lending arm, formerly Wells Fargo Dealer Services, maintains a centralized titling office at P.O. Box 168048, Irving, TX 75016. They are surprisingly flexible on Montana LLC requests as long as the borrower remains personally liable on the note. Wells Fargo will issue a “Letter of No Objection” upon request, which Montana accepts as authorization to title in the LLC’s name. Common rejection reason: incorrect spelling of the LLC name (Wells Fargo’s system is case-sensitive and requires exact match to the Articles of Organization).

Capital One Auto Finance

Capital One’s titling group, located at P.O. Box 660068, Dallas, TX 75266, has historically been one of the most accommodating major banks for Montana LLC transfers. They have a dedicated “Out-of-State Title Transfer” workflow accessible through their auto-loan customer portal. Approval typically takes 5 to 7 business days. Common rejection reason: missing a notarized member-consent statement when the LLC has multiple members.

Ally Financial

Ally is the largest indirect auto lender in the U.S. and processes roughly 25% of all dealer-financed transactions. Their titling office is at P.O. Box 8138, Cockeysville, MD 21030. Ally has a written Montana LLC policy that allows titling at origination if the dealer submits a “Commercial Title Request” form with the funding package. Once funded, transfers are harder, they require refinancing under the Ally Commercial Vehicle Loan program. Common rejection reason: dealer submitted the standard retail funding package instead of the commercial template.

Credit Unions: A Mixed Bag

Credit unions vary wildly. Navy Federal, PenFed, USAA, and Alliant participate in nationwide ELT systems and will typically allow Montana LLC titling with a member-resolution form. State-chartered community credit unions (under $1 billion in assets) often cannot title out of state due to charter restrictions and will require either payoff or refinance. Always call the credit union’s titling department before signing the loan documents to confirm Montana LLC compatibility.

Manufacturer Captives

Captive lenders, Ford Motor Credit, GM Financial, Toyota Financial Services, Honda Financial Services, BMW Financial Services, have their own quirks. Ford Credit and GM Financial generally accommodate Montana LLC titling for fleet customers but balk at one-vehicle retail transactions. BMW Financial Services and Mercedes-Benz Financial Services often require a full commercial-fleet application. Toyota Financial Services has the most retail-friendly Montana LLC process and will frequently approve at origination if the dealer flags the deal as “out-of-state titling” on the funding contract.

11. Commercial Loans vs. Personal Loans

The single biggest fork in the road for Montana LLC financing is whether you take out a personal auto loan or a commercial vehicle loan. The two products look superficially similar, you sign a promissory note, the bank perfects a lien, you make monthly payments, but the underwriting, documentation, and titling rules are completely different.

Personal Auto Loan

A personal loan underwrites you. The lender pulls your individual credit report (FICO Auto Score 8 or 9), evaluates your debt-to-income ratio, and decides whether to lend. The collateral is the vehicle, but the legal obligation is yours alone. Title is supposed to be in your personal name. Interest rates in 2026 typically run from 5.99% (excellent credit) to 14.99% (subprime). Loan terms range from 24 to 84 months.

Pros: Easy to qualify for, fast underwriting (often same-day approval at the dealership), low rates if you have great credit.

Cons: Most personal-loan contracts prohibit transferring the title to a third-party LLC without lender consent. The lender can call the loan due if they discover the transfer.

Commercial Vehicle Loan

A commercial loan underwrites the LLC. The lender will pull a Dun & Bradstreet report on the LLC, evaluate the LLC’s bank statements (or a personal guarantee if the LLC is new), and structure the loan with the LLC as borrower. Title is in the LLC’s name from day one. Interest rates run slightly higher, typically 6.99% to 16.99%, but you avoid the entire “transfer to LLC” headache.

Pros: Title automatically issued to the LLC, no due-on-sale risk, may qualify for Section 179 depreciation deductions if used in a real business, builds business credit.

Cons: Higher interest rates, more paperwork (Articles of Organization, EIN letter, operating agreement, sometimes financial statements), often requires personal guarantee anyway.

When the Bank Insists on Commercial

If your bank refuses to title an existing personal loan to a Montana LLC, your two practical options are: (1) refinance the personal loan into a commercial loan with the same bank or a new commercial lender, or (2) pay off the personal loan in cash, take possession of the title, and re-title to the LLC. Refinancing often makes more financial sense for vehicles under five years old. Cash payoff is the cleanest option for nearly-paid-off vehicles.

Where to Find a Commercial Vehicle Lender

Commercial vehicle financing is widely available. National players include Ally Commercial, Capital One Business, Wells Fargo Equipment Finance, Bank of the West, and U.S. Bank Equipment Finance. Specialty lenders like Crest Capital, Beacon Funding, and Balboa Capital cater to small-LLC customers and approve loans up to $250,000 with minimal documentation. Most commercial lenders close in 7 to 14 days and will work directly with Zero Tax Tags to coordinate the Montana titling.

12. Refinancing to Remove the Lien

Sometimes the cleanest path forward is to eliminate the lien altogether. If you have the cash, or can free up cash by tapping a HELOC, securities-backed line of credit, or cash-value life insurance loan, paying off the existing auto loan and re-titling to the Montana LLC is dramatically simpler than fighting with the bank.

Step-by-Step Cash Payoff and Retitle

- Request a 10-day payoff quote from your current lender. The quote should specify the exact dollar amount needed to satisfy the loan, including per-diem interest through a specific date.

- Wire the payoff funds to the bank’s payoff lockbox using the wiring instructions from the quote. Wire transfers process same-day; checks can take 5 to 7 business days to clear and apply.

- Wait for the lien release. The bank has 21 days under Montana law to file the release. For loans titled in another state, the release timeline depends on that state’s laws (usually 10 to 30 days).

- Receive the title. The originating state’s DMV will mail the lien-free title to you (or to the address on file) once the release is processed.

- Submit the clean title to Zero Tax Tags with your Montana LLC documents. We file the Montana title application, pay the $87.50 title fee plus registration, and get your new Montana title issued in the LLC’s name within 7 to 14 days.

Funding Sources for the Payoff

If you don’t have liquid cash sitting in checking, consider these payoff funding sources. A Home Equity Line of Credit (HELOC) typically charges prime + 0.5% to 2%, currently around 8% to 10%. A securities-backed line of credit (SBLOC) against a brokerage account can be as low as 5.5% to 7%. A 401(k) loan, up to $50,000 or 50% of vested balance, charges prime + 1% (around 8.5%) and you pay yourself back. Cash-value life insurance loans against permanent policies typically run 6% to 8% with no credit check and no fixed repayment schedule.

When Refinancing Makes More Sense Than Cash Payoff

If your vehicle is worth more than $75,000 and your current auto loan rate is below 7%, refinancing into a commercial loan in the LLC’s name is usually cheaper than tying up cash. The interest differential between paying cash (opportunity cost = 8-10% market returns) versus carrying a 7% loan typically favors keeping the loan. Run the math with your CPA before committing to a strategy.

13. 3 Detailed Case Studies

Theory is one thing. Real client outcomes tell the story better. Here are three actual Zero Tax Tags case studies (names changed) showing how lienholder issues get resolved when you have the right team behind you.

Case Study 1: The Texas Truck Buyer with a Chase Loan

Marcus, a 42-year-old contractor in Houston, Texas, ordered a 2026 Ford F-450 Platinum dually with the goal of registering it through a Montana LLC. The truck stickered at $112,000. Texas would have charged him $7,000 in sales tax plus $325 in title and registration fees. Marcus financed the truck through Chase Auto, which the dealer pre-approved at 6.49%.

When Marcus’s dealer F&I manager tried to fund the loan with the Montana LLC as titled owner, Chase rejected the funding package and demanded the title be in Marcus’s personal name. Chase’s compliance team flagged the deal as a potential straw purchase because the LLC had been formed only 30 days earlier through a Montana registered agent.

The Solution: Zero Tax Tags coordinated a three-way call with Chase Auto’s commercial titling group, Marcus’s CPA, and the dealer. We provided Chase with: (a) Marcus’s signed personal guaranty for the loan, (b) a copy of the LLC’s EIN letter from the IRS, (c) a notarized statement that the truck would be used in Marcus’s contracting business, and (d) a Montana titling-address verification letter. Chase approved the deal as a “commercial titling exception” and funded the loan with the title in the LLC’s name. Marcus saved $7,000 in Texas sales tax, paid $899 in Year 1 fees to Zero Tax Tags, and his 5-year total cost of Montana registration came in at $1,979 versus what would have been over $9,000 in Texas taxes and renewal fees.

Case Study 2: The California Luxury SUV Buyer with Dealer Financing Transferred to a Regional Bank

Linda, a 58-year-old retired physician in San Diego, bought a 2026 Range Rover Autobiography for $156,000. California would have hit her with $13,650 in sales tax (8.75% combined state and local) plus $1,200 in annual VLF fees for the first year. Her dealer originated the loan through Mountain America Credit Union, which then sold the loan to a regional California bank within 30 days of funding.

The first lender was fine with Montana LLC titling. The second lender (which acquired the loan) was not. Linda received a letter 45 days after delivery demanding she “correct” the title back to her personal name in California within 30 days, or the loan would be accelerated.

The Solution: We immediately filed a Notice of Loan Assumption with the new lender, attaching Linda’s original loan documents showing that her dealer-originated lender had consented to Montana LLC titling. Under California Commercial Code § 9404, a loan assignee takes the loan subject to defenses available against the original lender. Because Mountain America had originally consented, the regional bank could not unilaterally revoke that consent. The bank backed down within 14 days. Linda kept her Montana title, kept her loan, and kept the $13,650 in California sales tax in her own pocket.

Case Study 3: The Colorado RV Buyer with a Credit Union That Refused

Jim and Patricia, a 65-year-old couple in Denver, purchased a 2026 Newmar Dutch Star 4081 motorhome for $487,000. Colorado would have charged $14,610 in state sales tax (3% on RVs over $30,000) plus a 2.9% local tax adding another $14,000+ for a total tax bill north of $28,000. They financed $400,000 through their longtime credit union, Bellco Credit Union.

Bellco refused to title the motorhome in a Montana LLC. Their charter only allows them to perfect liens in Colorado, Wyoming, and New Mexico. There was no exception process and no escalation path. Jim and Patricia faced a choice: pay the $28,000 in Colorado taxes or find another lender.

The Solution: Zero Tax Tags introduced them to a national RV finance specialist (Essex Credit, a division of Bank of the West) that offers Montana LLC titling at origination on motorhome loans. Essex approved a refinance at 7.49% with the Montana LLC as the borrower. The refinance closed in 18 days. Jim and Patricia paid off Bellco, got the clean Colorado title, transferred to Montana through the LLC, and saved over $26,000 in net taxes after accounting for refinancing costs and the Year 1 Zero Tax Tags fee. Their 5-year total Montana registration cost: $1,979. Their lifetime savings on this single motorhome: well over $30,000 once future renewals are factored in.

Lesson from all three cases: Lender objections look intimidating but rarely survive a structured, documented response. Every major obstacle in these case studies was overcome with paperwork, not with confrontation, not with threats, just with the right form filled out the right way and sent to the right person.

14. Troubleshooting: When the Bank Won’t Budge

Here are six common scenarios we see at Zero Tax Tags and how to handle them. The first three are the original “big three” troubleshooting cases. The next three are advanced scenarios that have emerged as Montana LLC registrations have become more common.

Scenario A: Bank Refuses to Release MCO/Title

You are trying to transfer a car you already own (but financed) from Texas to Montana. The Texas title is held by the bank. The bank says, “We won’t release the title until the loan is paid.”

The Solution:

You need to file a Request for Foreign Title Transfer.

This form is a formal request from the state of Montana to your lender. It tells them: “We aren’t trying to steal your collateral; we just want to register it here. Please send the title to the County Treasurer, we will record your lien, and send the new Montana title back to you.” Most banks comply once they understand the new title will still bear their lien.

Scenario B: Dealer Never Sent MCO to Lender

You bought the car, drove it home, and 90 days later, you still have no plates. The dealer says “We sent the paperwork.” The Montana DMV says “We have nothing.”

The Reality:

The dealer likely messed up the “perfection” fee or the address. They might be sitting on the MCO because they don’t know how to fill out the Montana forms.

The Solution:

Demand proof of mailing. If they haven’t sent it, instruct them to send the MCO directly to the Vehicle Services Bureau in Helena with the required $8 lien filing fee. If they refused to pay the $8, the state threw the application in the trash.

Scenario C: Lender Lost the MCO

It happens more than you think. The dealer sent it, the bank got it, and then… it vanished.

The Solution:

This enters the territory of a Bonded Title.

If the MCO is gone, you cannot prove ownership. You may have to apply for a Break/Bond Title.

- You will need a VIN inspection.

- You will need to buy a surety bond for 1.5x the value of the vehicle.

- Montana holds this bond for 3 years to protect against claims that the vehicle was stolen.

Scenario D: Insurance Company Refuses to Bind LLC Coverage

Your bank requires comprehensive and collision coverage with them listed as loss payee. You apply for a commercial auto policy in the LLC’s name, but the insurer refuses to issue it because the LLC has no operating history, no commercial drivers, and no business location in Montana.

The Solution:

Use a specialty broker who writes “non-business commercial” auto policies for Montana LLCs. Companies like Foremost, Progressive Commercial, and Hagerty (for collector vehicles) have niche programs designed specifically for single-vehicle LLC ownership. Premiums typically run 10% to 25% higher than personal coverage but the LLC name appears on the declarations page, satisfying the bank’s requirement.

Scenario E: Loan Servicer Sells Your Loan Mid-Transfer

You start the Montana LLC retitle process with the original lender, who consented in writing. Halfway through the process, your loan is sold to a different servicer who refuses to honor the consent.

The Solution:

Invoke the assignment-of-defenses rule under your state’s Uniform Commercial Code (typically UCC § 9-404). The new servicer takes the loan subject to all defenses and consents that existed at the time of the assignment. Send the new servicer a certified letter attaching the original consent letter, citing the relevant UCC section, and demanding they honor the prior agreement. This works in 80%+ of cases.

Scenario F: Montana DMV Rejects Lien Recording for Out-of-State Lender

Your application gets sent back from Helena because the lienholder name doesn’t match a Montana-registered Secured Party Index entry.

The Solution:

The lender needs to register as a Secured Party with the Montana Secretary of State (or use a registered agent for that purpose). National banks usually have this taken care of. Smaller out-of-state lenders may not. If the lender refuses to register, the workaround is to add an authorized Montana agent to the lien notation, with the lender’s name in parentheses. Zero Tax Tags handles this filing routinely.

More MCO Solutions: For additional help with dealer-related MCO issues, see our guide on What to Do When the Dealer Won’t Release Your MCO and Out-of-State MCO Requirements.

Summary

Transferring a title with a lienholder isn’t impossible, but it is bureaucratic warfare. The bank wants to protect their money. The state wants their $8 filing fee. You want your Zero Tax Tag. Every player in this three-way dance has a different priority, and a single missed signature, fee, or address line can stall your registration for weeks or months.

The good news: every obstacle in this guide, from the dealer who doesn’t know Montana paperwork, to the bank that refuses out-of-state titling, to the credit union that won’t release a charter-restricted lien, to the DMV that rejects a packet over an $8 fee, has a documented solution. Thousands of Zero Tax Tags clients have walked this path and come out the other side with Montana plates on their truck and tens of thousands of dollars in tax savings in their pocket.

If you miss one signature, one fee, or one address line, your application enters the void. Don’t fight the banks and the DMV alone. Our flat-fee structure, $899 in Year 1 (which includes the $699 service fee plus $200 LLC formation), $270 per year for renewals after that, with a five-year total of $1,979 for vehicles under $150,000, is a fraction of what most clients save in a single year of avoided sales tax.

Ready to Navigate Your Title Transfer with Lienholder?

Montana LLC registration with a lienholder is complex. Let Zero Tax Tags handle the three-way dance between you, the state, and your bank. We’ve perfected thousands of liens, yours is next.